Market movements this week were dominated by currency related headlines. Rupee has slumped lower versus dollar and has raised the fears of inflation making a comeback via expensive imports. The selling, which was till recently going on in large cap stocks has spread to midcap stocks as well. Sensex ended this week with a loss of 1.3%, while Nifty and CNX Midcap lost 1.2% and 4.0% respectively.

Monday - Sensex up by 0.1%, Nifty down by 0.1%, Midcap down by 1.3%

Market traded under the pressure of depreciating currency. Rupee touched a low of 58 versus dollar and stoked inflation fears among the investors. IT stocks went higher will most of the midcap stocks slumped as currency traded lower.

Tuesday - Sensex down by 1.5%, Nifty down by 1.5%, Midcap down by 1.9%

Markets sentiments continued to be weighed down by currency depreciation. Recent good news from RBI related to decline in inflation as shown by downward movement in WPI and CPI have been totally offset by fears of inflation strengthening again as rupee continues to slide against the dollar. FIIs continued to sell Indian bonds as yield difference with US bonds lessen.

Wednesday - Sensex down by 0.5%, Nifty down by 0.5%, Midcap down by 0.4%

Markets were volatile as the rupee found support in the Economic Affairs Ministry's comments that the fall is a temporary phase and news that RBI has intervened by selling dollars. There were also reports that govt may raise FDI limits to finance CAD.

India also released its IIP and CPI numbers. While IIP growth came lower at 2% in April vs 3.4% in March, May CPI came in at 9.31% vs 9.39% in April. Decline in IIP growth has raised concerns whether RBI will cut rates in an attempt to stimulate growth although RBI's hands will be tied as rupee continues its slump.

Thursday - Sensex down by 1.1%, Nifty down by 1.1%, Midcap down by 1.9%

Market traded lower as selling continued among no rate cut hopes, rising CAD and higher inflationary expectations.

Friday - Sensex up by 1.9%, Nifty up by 1.9%, Midcap up by 1.4%

Markets took a reprieve from continuous selling it was witnessing from past few sessions as investors hinged their hopes on rate cut from RBI next week after May WPI came lower at 4.7%.

Friday, June 14, 2013

Friday, June 7, 2013

Weekly Market Commentary - Jun 3 - Jun 7, 2013

This week may seem to be a non-event for the markets on the onset but one major step taken by the Govt recently will go a long way in consolidating its fiscal position. Govt launched inflation indexed bonds. IIBs, as they are called, in an attempt to wean off local investors from gold. Gold, one of the crucial components of our trade deficit has been touching new highs as markets turned volatile, giving the establishment new headache every passing day. How far will IIB go in reducing the country's gold import bill, only time will tell. You can read about IIB here.

Monsoon is here. On June 1, it arrived in Kerala, two days ahead of its time. It is a well known fact that the monsoon rains are very crucial for India, one of the world's largest producers and consumers of food.

Sensex ended this week with a loss of 1.7%, while Nifty and CNX Midcap lost 1.8% and 0.2% respectively.

Monday - Sensex down by 0.8%, Nifty down by 0.8%, Midcap down by 0.1%

Markets continued its downward movement taking the cues from sub 5% GDP growth announced previous week, weakening in rupee and from the fact that FIIs were net sellers on Friday. The sentiment were further dampened by the results of private survey, PMI, conducted by HSBC which indicated slowdown in manufacturing activity. The survey, which measures the business activity in Indian factories excluding utilities, indicated that index eased to 50.1 in May 2013 from 51 in April 2013, due to fall in output and less new orders. The survey also suggested that employment rose at a slightly faster pace; input prices deflated and output prices declined for the first time since the global financial crisis.

In data released by govt after trading hours on Friday, fiscal deficit for FY13 came in lower at 4.9% of GDP against 5.2% budgeted (revised) in Feb 2013. Fiscal deficit for FY14 is budgeted at 4.8% of GDP.

Tuesday - Sensex down by 0.3%, Nifty down by 0.3%, Midcap up by 0.4%

Markets lost initial gains made earlier in the day as rupee strengthened a bit and ended slightly negative amidst the choppy trade marked by profit booking.

Wednesday - Sensex up by 0.1%, Nifty up by 0.1%, Midcap up by 0.3%

No strong movements occur during the day. Markets ended slightly up as investors turn to bottom fishing, bargain hunting as markets in other parts of Asia see heavy selling due to fear of reduction in stimulus spending from Fed.

Thursday - Sensex down by 0.2%, Nifty down by 0.0%, Midcap down by 0.1%

Absence of any big news flow kept the sensex rangebound. RIL's AGM previous day, was a dull affair with no big bang announcements. Mukesh Ambani made familiar noises about E&P and 4G business.

Friday - Sensex down by 0.5%, Nifty down by 0.7%, Midcap down by 0.8%

Markets are trading nervous as rupee seems to be heading southward. Global environment has turned cautious after Fed's indication of tapering of its stimulus spending in case US economy gains upward momentum.

Monsoon is here. On June 1, it arrived in Kerala, two days ahead of its time. It is a well known fact that the monsoon rains are very crucial for India, one of the world's largest producers and consumers of food.

Sensex ended this week with a loss of 1.7%, while Nifty and CNX Midcap lost 1.8% and 0.2% respectively.

Monday - Sensex down by 0.8%, Nifty down by 0.8%, Midcap down by 0.1%

Markets continued its downward movement taking the cues from sub 5% GDP growth announced previous week, weakening in rupee and from the fact that FIIs were net sellers on Friday. The sentiment were further dampened by the results of private survey, PMI, conducted by HSBC which indicated slowdown in manufacturing activity. The survey, which measures the business activity in Indian factories excluding utilities, indicated that index eased to 50.1 in May 2013 from 51 in April 2013, due to fall in output and less new orders. The survey also suggested that employment rose at a slightly faster pace; input prices deflated and output prices declined for the first time since the global financial crisis.

In data released by govt after trading hours on Friday, fiscal deficit for FY13 came in lower at 4.9% of GDP against 5.2% budgeted (revised) in Feb 2013. Fiscal deficit for FY14 is budgeted at 4.8% of GDP.

Tuesday - Sensex down by 0.3%, Nifty down by 0.3%, Midcap up by 0.4%

Markets lost initial gains made earlier in the day as rupee strengthened a bit and ended slightly negative amidst the choppy trade marked by profit booking.

Wednesday - Sensex up by 0.1%, Nifty up by 0.1%, Midcap up by 0.3%

No strong movements occur during the day. Markets ended slightly up as investors turn to bottom fishing, bargain hunting as markets in other parts of Asia see heavy selling due to fear of reduction in stimulus spending from Fed.

Thursday - Sensex down by 0.2%, Nifty down by 0.0%, Midcap down by 0.1%

Absence of any big news flow kept the sensex rangebound. RIL's AGM previous day, was a dull affair with no big bang announcements. Mukesh Ambani made familiar noises about E&P and 4G business.

Friday - Sensex down by 0.5%, Nifty down by 0.7%, Midcap down by 0.8%

Markets are trading nervous as rupee seems to be heading southward. Global environment has turned cautious after Fed's indication of tapering of its stimulus spending in case US economy gains upward momentum.

Wednesday, June 5, 2013

Inflation Indexed Bonds - Real risk of good intentions turning into bad economics?

Indian FM, in its current pursuit to contain fiscal deficits, have taken certain strong measures. One of the important steps taken is introduction of inflation linked bonds. FM is desperately trying to wean off Indian investors from their insatiable demand for gold which is widely considered a hedge against inflation and one of the main culprits behind rising deficits.

Govt earlier tried to discourage the gold demand by raising the import duty from 2% to 6% in beginning of this year but met with little success. Gold recently sent a shocker down the Govt spine when Apr statistics indicated a 138% jump in gold imports to $7.5 billion, taking the current account deficit to $17.8 billion from $10.3 billion in March.

Govt now is re-attempting to provide an alternative investment route in the form of inflation linked bonds to protect the investors against rising prices. In its earlier attempt in 1997, Govt offered protection to only principal payment. But this time, it went one step ahead and offered interest income to be also indexed to protect against inflation.

RBI's bond sale on Tuesday was a success as the corporates lapped up the product. Issue will open for retail investors in October this year.The main selling point is an offer of 1.44% real yield over the final WPI, with almost four months lag period, which means current offer is linked to January 2013 WPI rate.

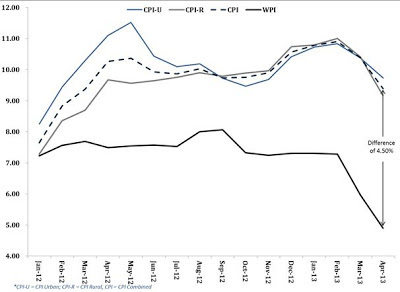

There are two major issues with the current bond sale. First, the debt is indexed to WPI, which we know calculates the price changes in the trades among the corporates NOT consumers or retail investors. This essentially means, bond does not provides consumers protection against the rising prices, what best it does is provide partial protection. There is almost 4.5% difference between current WPI and CPI numbers. Though, it is too early to speculate on its impact on gold demand, I am not sure replacing WPI with CPI as the inflation benchmark in the offer would have served the purpose of streamlining the Govt finances.

Second major issue is, which is really a downside, what happens if, we faltered on our path to regain the lost growth, FII flows dries up due to some reason and we are left with falling currency, which fires up the inflation and inflationary expectations in domestic economy and Govt is left with huge bonds liability in a slow growth environment which will raise Govt borrowing costs and inturn stoke further inflation. Nobody on the street is seem to be discussing this.

What all I know is, global economy is not out of mess, markets are been artificially inflated with central bankers printing huge quantity of money, commodity prices are down - not because of increasing competition or supply but decline in demand across the developed countries and every important economy is struggling to get growth back on its feet.

Govt earlier tried to discourage the gold demand by raising the import duty from 2% to 6% in beginning of this year but met with little success. Gold recently sent a shocker down the Govt spine when Apr statistics indicated a 138% jump in gold imports to $7.5 billion, taking the current account deficit to $17.8 billion from $10.3 billion in March.

Govt now is re-attempting to provide an alternative investment route in the form of inflation linked bonds to protect the investors against rising prices. In its earlier attempt in 1997, Govt offered protection to only principal payment. But this time, it went one step ahead and offered interest income to be also indexed to protect against inflation.

RBI's bond sale on Tuesday was a success as the corporates lapped up the product. Issue will open for retail investors in October this year.The main selling point is an offer of 1.44% real yield over the final WPI, with almost four months lag period, which means current offer is linked to January 2013 WPI rate.

There are two major issues with the current bond sale. First, the debt is indexed to WPI, which we know calculates the price changes in the trades among the corporates NOT consumers or retail investors. This essentially means, bond does not provides consumers protection against the rising prices, what best it does is provide partial protection. There is almost 4.5% difference between current WPI and CPI numbers. Though, it is too early to speculate on its impact on gold demand, I am not sure replacing WPI with CPI as the inflation benchmark in the offer would have served the purpose of streamlining the Govt finances.

Second major issue is, which is really a downside, what happens if, we faltered on our path to regain the lost growth, FII flows dries up due to some reason and we are left with falling currency, which fires up the inflation and inflationary expectations in domestic economy and Govt is left with huge bonds liability in a slow growth environment which will raise Govt borrowing costs and inturn stoke further inflation. Nobody on the street is seem to be discussing this.

What all I know is, global economy is not out of mess, markets are been artificially inflated with central bankers printing huge quantity of money, commodity prices are down - not because of increasing competition or supply but decline in demand across the developed countries and every important economy is struggling to get growth back on its feet.

Friday, May 31, 2013

Weekly Market Commentary - May 27 - May 31, 2013

We started the week with big bang news of another potentially huge discovery in KG-D6 by RIL and ended the week with weak, but expected sub 5% 4Q GDP numbers.

In the context of current Indian market performance, you can safely say that current volatility is the by-product of easy liquidity and uncertain economic environment. Every new economic data brings with it the question everyone is asking, whether this is the last of the bad news we are receiving. With every data release, we hear experts talking about Indian market bottoming out. But have we?

Current GDP figures are at decade low, consumption is showing decline, rupee is falling, RBI is dithering on rate cuts and Indian investor is choosing to stay away from stocks making our markets even more vulnerable to sudden FII outflow which could prove disastrous to the economy. This week sensex made a small gain of 0.3% while Nifty and CNX Midcap ended flat.

Monday - Sensex up by 1.7%, Nifty up by 1.7%, Midcap up by 1.2%

Sensex zoomed past 20K mark, gaining more than 350 points in the process. Main catalyst was Reliance Industries late Friday announcement of big gas discovery in KG D6 basin. Company is planning to start appraisal drilling soon to ascertain the amount of gas discovered. It remains to be seen how much of this gas, Reliance, can actually drill out commercially. Discovery also gives Reliance an additional weapon to strongly pursue market pricing of gas with govt. RIL, along with its partner BP are currently negotiating for higher price for their KG-D6 gas which is strongly contested by Petroleum Ministry and Fertilizer Ministry. There was also some short covering seen in the market, as current F&O contract expires this week.

Tuesday - Sensex up by 0.6%, Nifty up by 0.5%, Midcap up by 0.6%

Markets remained cautious ahead of GDP data announcement on Friday. Coal India, country's largest coal supplier, which reported earnings post market hours previous day, reported a jump of 35%, beating the consensus estimates, on the back of higher supplies and lower employee expenses. Company also announced its decision to hike prices by 10%.

Wednesday - Sensex down by 0.1%, Nifty down by 0.1%, Midcap down by 0.6%

No major movements in Sensex, as markets focus on Friday GDP data announcement and F&O expiry. Sun Pharma, country's top drugmaker by market value, reported 23% rise in 4Q profits and announced a bonus share issue.

Thursday - Sensex up by 0.3%, Nifty up by 0.3%, Midcap down by 0.1%

Sensex made small gain as investors cover up their position on the day of F&O expiry. Tata Motors and Mahindra & Mahindra beat the consensus estimates while ONGC reported a decline in 4Q profit on the back of lower sales and higher payment on statutory levies.

Friday - Sensex down by 2.3%, Nifty down by 2.3%, Midcap down by 1.0%

Markets went downhill as GDP grew at mere 4.8% in 4Q and 5% for full fiscal year 2013. Though, the street was expecting sub 5% GDP figure for 4Q, it was the comments from RBI which set the bearish tone pushing the investors towards the exit. RBI governor maintained it cautious stance suggesting that inflation data still has upward risk while current account position stays out of comfortable range. These comments deprived the market of any rate cut hopes in June meeting and led to selling across the board. Rupee also took the hit and is trading now at close proximity of 57 to a dollar.

In the context of current Indian market performance, you can safely say that current volatility is the by-product of easy liquidity and uncertain economic environment. Every new economic data brings with it the question everyone is asking, whether this is the last of the bad news we are receiving. With every data release, we hear experts talking about Indian market bottoming out. But have we?

Current GDP figures are at decade low, consumption is showing decline, rupee is falling, RBI is dithering on rate cuts and Indian investor is choosing to stay away from stocks making our markets even more vulnerable to sudden FII outflow which could prove disastrous to the economy. This week sensex made a small gain of 0.3% while Nifty and CNX Midcap ended flat.

Monday - Sensex up by 1.7%, Nifty up by 1.7%, Midcap up by 1.2%

Sensex zoomed past 20K mark, gaining more than 350 points in the process. Main catalyst was Reliance Industries late Friday announcement of big gas discovery in KG D6 basin. Company is planning to start appraisal drilling soon to ascertain the amount of gas discovered. It remains to be seen how much of this gas, Reliance, can actually drill out commercially. Discovery also gives Reliance an additional weapon to strongly pursue market pricing of gas with govt. RIL, along with its partner BP are currently negotiating for higher price for their KG-D6 gas which is strongly contested by Petroleum Ministry and Fertilizer Ministry. There was also some short covering seen in the market, as current F&O contract expires this week.

Tuesday - Sensex up by 0.6%, Nifty up by 0.5%, Midcap up by 0.6%

Markets remained cautious ahead of GDP data announcement on Friday. Coal India, country's largest coal supplier, which reported earnings post market hours previous day, reported a jump of 35%, beating the consensus estimates, on the back of higher supplies and lower employee expenses. Company also announced its decision to hike prices by 10%.

Wednesday - Sensex down by 0.1%, Nifty down by 0.1%, Midcap down by 0.6%

No major movements in Sensex, as markets focus on Friday GDP data announcement and F&O expiry. Sun Pharma, country's top drugmaker by market value, reported 23% rise in 4Q profits and announced a bonus share issue.

Thursday - Sensex up by 0.3%, Nifty up by 0.3%, Midcap down by 0.1%

Sensex made small gain as investors cover up their position on the day of F&O expiry. Tata Motors and Mahindra & Mahindra beat the consensus estimates while ONGC reported a decline in 4Q profit on the back of lower sales and higher payment on statutory levies.

Friday - Sensex down by 2.3%, Nifty down by 2.3%, Midcap down by 1.0%

Markets went downhill as GDP grew at mere 4.8% in 4Q and 5% for full fiscal year 2013. Though, the street was expecting sub 5% GDP figure for 4Q, it was the comments from RBI which set the bearish tone pushing the investors towards the exit. RBI governor maintained it cautious stance suggesting that inflation data still has upward risk while current account position stays out of comfortable range. These comments deprived the market of any rate cut hopes in June meeting and led to selling across the board. Rupee also took the hit and is trading now at close proximity of 57 to a dollar.

Subscribe to:

Posts (Atom)